This article examines the implications of the contracts between the four main South African supermarkets and their SME suppliers. Supermarkets’ procurement practices, in particular their practice of charging suppliers a substantial ‘rebate commission’ as well as requiring suppliers to comply with private, rather than public, production and health standards, have a significant impact on the ability of new SME suppliers to enter the market and to create jobs. This has important policy implications.

Introduction

In the short-to-medium term, states the National Development Plan (NDP), approximately 90% of the projected semi- and low-skilled jobs are most likely to be created by ‘small and expanding firms’ that service the domestic market (NDP 2012:118). Agro-processing is identified as a key sector. As both the NDP and Philip (2010) underline, however, the production of commodity foodstuffs is highly concentrated among a few large suppliers. Indeed, mass-consumed goods, including basic foodstuffs, clothing and household detergents, are produced mostly by large suppliers whose supply chains are vertically integrated. These suppliers can cut their margins per unit, which ‘tends to squeeze out even medium-sized competitors, let alone small producers’ (Philip 2010: 15).

A question is whether product lines which are not dominated by large suppliers could be a source of employment creation. One possibility is high-value foodstuffs such as special oils, and pre-prepared foods. This article reports on a recent study (Von Broembsen 2016) which investigates the relationships between SME suppliers of high-value foodstuffs and the four main supermarkets – Pick n Pay, Shoprite Checkers, Woolworths and Spar. It shows that factors such as bargaining power, branding, procurement and contracting practices, automation, and quality and hygiene standards can have a decisive effect on the competitiveness, viability and job-creation potential of small suppliers. These findings have important policy implications.

The nature of the study and the profile of the interviewees

The study surveys 28 suppliers to the four supermarkets, two senior executives from two of the supermarkets, an ex-buyer from one of the supermarkets (now a consultant to SME suppliers), a packaging company and a driver for one of the suppliers. The interviewees were identified in three ways: through a database of approximately 80 small suppliers in the Western Cape; by suppliers introducing me to other suppliers; and by identifying products on supermarket shelves and cold-calling the suppliers. SME suppliers which supplied more than one supermarket were selected over those that supplied only one supermarket. The individuals were interviewed using a semi-structured questionnaire, followed by an open-ended discussion.

The SME suppliers of high-value foodstuffs had the following profile:

- Approximately 85% of the SMEs were older than 5 years. Most of them had started as an informal enterprise that operated from a garage or kitchen. This makes the study relevant for assessing the potential for informal-sector suppliers to expand and develop linkages to formal-sector supermarkets.

- Their annual turnover ranged from below R1 million to over R20 million. Three were below R1 million, ten between R1 million and R10 million, three between R10 million and R20 million, and five over R20 million.

- Generally, the larger the supplier firm in terms of turnover, the more employees it has. The average employment was approximately 40. Eight firms employed fewer than 20 workers. Almost half of the firms had between 21 and 60 employees. Only four suppliers employed over 60 workers, the largest having 285 employees. The firms that employed fewer than ten people tended to be either highly automated or involved only in packaging and distribution. On average, suppliers employed five skilled employees and approximately 35 unskilled employees. Surprisingly, no casual, seasonal or temporary workers were employed.

Differences between the four supermarkets: suppliers’ perspectives

Interviewees reported that Spar is an important entry point to test the market. Since Spar operates as a franchise, franchisees of stores have some discretion with regard to procurement and can decide to stock a particular product and contract directly with a supplier. Thus SME suppliers can produce small quantities and supply just one store (which also means that they avoid charges, known as ‘rebate commissions’, which the large supermarkets levy; this is explained below).

Given that Spar has a relatively small market share, growth beyond a certain size depends on SMEs supplying other supermarkets too. Shoprite Checkers is a favourite because its shelf prices are lower than those of other supermarkets (thus products sell quicker). However, since its primary market is a lower-income segment of the population, the market for high-value products has a ceiling. Woolworths has the largest scope, but it is difficult to become a supplier because most of its products are ‘private label’ (i.e. suppliers’ products are sold under the Woolworths brand).

This means that supplying Pick n Pay is critical to the growth of emerging small suppliers. The research suggests that Pick n Pay abuses this market power when contracting with SMEs’ suppliers that do not have a strong, independent brand.

The nature of the contracts between supermarkets and SME suppliers

Retailers use two legal mechanisms to exercise control over production and supply by SME firms that are legally autonomous: supply contracts; and production and hygiene standards. The typical supply contract between the supermarkets and their SME suppliers outlines the basis on which the supermarket places orders. The supermarket and the supplier agree on a supply price and the supermarket’s mark-up for each product, i.e. determining the selling (or shelf) price. Few suppliers take issue with this process.

The complicating factor is that, whilst the supplier nominally receives payment based on the agreed supply price, all four supermarkets charge their SME suppliers a ‘rebate commission’ – a percentage ranging between 6% and 16% of every order. The rebate commission comprises several different fees:

- An ‘incentive fee’, usually around 5% of the value of an order, is a fee that the supplier pays to the supermarket simply for the privilege of having the supermarket stock their product.

- An advertising fee, which is notionally charged for advertising, but without a legal obligation on the supermarket to advertise the supplier’s product(s).

- A settlement fee, which is a fee to ensure that the supermarket pays the supplier within 30 days of receipt of goods.

- A ‘swell allowance’, charged only by Pick n Pay, for it to carry the risk of over-ordering stock and damage to the stock after delivery (even if the damage is caused by Pick n Pay).

There is little variation among the supermarkets in the rebate commissions, but there appears to be a huge variation among the charges paid by different SMEs and the service received from the supermarket. For example, some suppliers did not pay any rebate commission at all and were paid for a delivery within seven days. Other suppliers paid a 10% rebate commission, but were only paid within 30 days. All except two suppliers were unaware that they had been contracted on different terms to those that applied to competitors.

In addition to the rebate commission, Pick n Pay terms of trade include the following:

- An obligation on the part of the supplier to contribute approximately R1 500 per store for the refurbishment of existing stores or the building or acquisition of new stores. Technically, suppliers are meant to pay only if the relevant store will stock its products, but suppliers reported that they had to contribute to stores that do not even stock their products.

- A stipulation that promotion costs (such as offering discounts or two for the price of one) are borne by the supplier, while Pick n Pay decides unilaterally which products are to be promoted.

- A penalty that is triggered if a supplier fails to deliver a certain percentage – usually 95% – of orders over a period of a year, irrespective of the reason for non-delivery.

Suppliers complain that Pick n Pay is unwilling to take the reasons for non-delivery of orders into account, even when non-delivery is because of Pick n Pay’s faulty refrigeration facilities, for example, or because the products are not in season.

The basis for the penalties levied by Pick n Pay’s seems like a clear example of the supermarket abusing its market power. While the penalty clause is based on a year’s supply and penalises the supplier for its failure to deliver over that period, the supplier has no corresponding claim that the supermarket has to take delivery of ordered supplies and pay according to agreed terms for the year. According to the suppliers, Pick n Pay simply claims that it is contracting afresh for each specific order it places – and thus can decide to place an order or not as it wishes, without suppliers having any recourse.

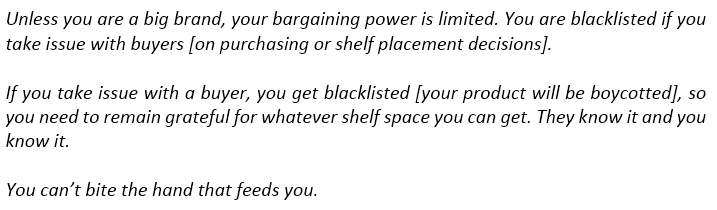

Suppliers generally report that they are unable to contest their contract terms, as they will simply be ‘blacklisted’ and their products ‘de-listed’ and no longer stocked by a supermarket. Below are typical comments made by suppliers, illustrating the enormous power that supermarkets enjoy:

Pick n Pay’s penalty practice, together with the threat of being ‘delisted’ for even non-commercial reasons (such as questioning decisions), creates a profound insecurity of contract and a huge risk for suppliers. It fundamentally limits a supplier’s incentive to invest in new capacity to expand output and create more, or better-paid, jobs.

The practices detailed above mirror supermarket practices that pass risks to their suppliers in the United Kingdom (UK), which were found to be uncompetitive by the UK Competition and Market Authority. The UK Authority’s report highlights circumstances ‘where allocations of risk may be agreed up-front between a retailer and supplier, but that the extent of risk transferred to the supplier was excessive (UK Competition Commission 2006: 15).

The implications of private production and hygiene standards for SMEs

Three government departments – Health (DOH), Agriculture, Forestry and Fisheries (DAFF) and Trade and Industry (DTI) – regulate and enforce food safety in South Africa. Six Acts govern the production, manufacture, transport and labelling of food manufacture (Siphugu 2011). In addition, the international Hazard Analysis Critical Control Point (HACCP) system has been gazetted as part of the Foodstuffs, Cosmetics and Disinfectants Act; however, no sector is yet legally obliged to implement HACCP.

All four supermarkets have historically required compliance with these public health and safety standards. However, in recent years, Woolworths, Pick n Pay and Shoprite Checkers have started to require strict compliance with stringent private production and hygiene standards. (Spar only requires a certificate of compliance from the DOH, or compliance with either HACCP or Woolworths’s audits.)

The big three supermarkets argue that compliance with the private standards are necessary for consumer protection. One has to question this assertion, since Spar’s products comply with public standards and consumers are safe. And, as Dolan and Humphrey (2000) argue, standards often are a manifestation of relative power rather than a desire to protect consumers. For example, UK Supermarkets demand compliance from African suppliers but not from Spanish suppliers, whose products they do stock (which undermines their justification that the private standards are there to protect consumers). All over the world compliance costs for suppliers are considerable and have the effect of excluding new market entrants (Gereffi & Lee 2012; Navdi 2008).

Interviewees reflected that, if it weren’t for Spar, these compliance costs would prevent new SME suppliers that do not have considerable capital from starting-up. All interviewees favoured a mandatory period of grace for start-up businesses to attain gradual compliance (which Woolworths does with its private-label suppliers).

Conclusion and policy implications

The key findings are, first, that the opportunities for SMEs to grow are circumscribed by the SME supplier’s bargaining power relative to a supermarket. The majority are without a powerful brand and have little to no bargaining power. Secondly, the fact that supermarkets centralise their procurement, that they impose contracts on their SME suppliers and often abuse their market power undermines the growth and job creation potential of SMEs. Thirdly, because their contracts are insecure and supermarkets’ proclivity to pass risks to suppliers through rebate commissions, suppliers choose to automate rather than employ more people or up-skilling their staff. Finally, the rise of private production and hygiene standards, and the costs of compliance have a chilling effect on SME entrants.

These procurement practices – which have been found to transgress Competition Law in the UK – have profound implications for the viability and growth of small businesses in the food industry, which creates jobs for many unskilled workers. These practices will have to be addressed, for example by the Competition Commission, if the NDP’s vision is to be realized.

I argue for policy interventions in three areas. First, the state should regulate the contracts between supermarkets and small suppliers as it does other relationships marked by unequal power relations, for example contracts between retailers and consumers, employers and employees, and franchisors and franchisees. (Following the UK example, an ombudsman should be considered as the best means to implement such a legislative intervention.) Secondly, government must regulate how private standards may be enforced, including provision for gradual compliance over a period of three to five years, and ensure that uncompetitive practices are eliminated. Thirdly, the practice of rebate commissions has to be scrutinised. Finally, SME suppliers should enjoy representation, as supermarkets do, on the SA Bureau of Standards (SABS), the retail committee of the National Empowerment Fund, and NEDLAC, which make policy decisions.

Written by Marlese von Broembsen, Centre for Law and Society, University of Cape Town, for Econ3x3

EMAIL THIS ARTICLE SAVE THIS ARTICLE ARTICLE ENQUIRY FEEDBACK

To subscribe email subscriptions@creamermedia.co.za or click here

To advertise email advertising@creamermedia.co.za or click here