A nationally representative survey of South African smokers confirms that illegal cigarettes made up roughly 60% of the total market in 2021. This aligns closely with other research indicating that the illicit market grew from less than 10% before 2010 to more than 55% in 2020 and subsequent years. We estimate the share of cigarettes sold at prices strongly indicative of illicit production, and identify brands and brand owners most implicated. The results show where enforcement agencies should focus their attention to curb the continued rise of illicit trade.

Introduction

South Africa’s cigarette illicit trade has reached crisis levels. Illicit trade reduces the excise tax revenue collected by the South African Revenue Services (SARS). It undermines public health policies by making cigarettes more affordable and easily accessible, particularly to low-income smokers who might otherwise not smoke.

South Africa’s illicit trade began to surge in 2010, when ultra-cheap, locally produced cigarettes started entering the market. This growth in illicit trade was accelerated by institutional failure at SARS between 2014 and 2018, when specialised enforcement units (including those responsible for illicit markets) were disbanded. In addition, South Africa’s five-month long Covid-19 tobacco sales ban in 2020 further entrenched illicit distribution networks. Even after the sales ban was lifted, illicit trade remained high. Studies using a variety of methods and data show that illicit trade increased from less than 10% of the cigarette market in 2010, to around 60% in 2022.

Using the 2021 South African Global Adult Tobacco Survey (GATS), we provide a national estimate of illicit trade and identify key illicit cigarette manufacturers. The data confirm that the illicit market was roughly 60% of the cigarette market in 2021.

Historically, multinational corporations (MNCs) dominated the market, with British American Tobacco having a more than 90% market share at the start of the century. This has changed dramatically in the 21st century. Local producers (non-MNCs) now have a collective market share of close to 60%, and almost exclusively sell under-taxed products.

Data and methods

We use South Africa’s first GATS survey, conducted in 2021. GATS is a standardised nationally-representative household survey on adult tobacco use. The sample included both smokers and non-smokers, aged 15 years and older. The data is weighted using the sample and consumption weights. Some observations are excluded due to non-response on consumption from non-daily smokers.

The questionnaire covers the respondent’s most recent cigarette purchase, and has questions on total cost, type of product packaging, and quantity purchased. Purchase information is used to calculate unit prices, which are then converted to a standardised 20-pack price.

There are several methods used to estimate illicit trade, such as gap analysis, empty pack collections, or the price threshold method (PTM). The basis of the PTM is that the retail price of a pack should be at least high enough to cover the taxes and non-tax price elements. We define the threshold price as the sum of the minimum tax and non-tax price elements (i.e. wholesale and retail margins). Illegal cigarettes are typically sold at very low prices, often even below the tax due per pack. A retail price that is close to or below the excise tax amount is a strong indicator of illicit activity. Since the non-tax elements are uncertain, we vary these estimates for a robust illicit trade estimate (hence why we have multiple thresholds described below).

During the 2021/2022 fiscal year, the excise tax was R18.79 per pack of 20 cigarettes, with 15% VAT payable on this amount, making the minimum tax R21.61 per pack. Based on several sources, including reports commissioned by the tobacco industry, the minimum manufacturing cost of a pack of cigarettes in 2021 was between R2.50 and R4.00. Wholesale and retail margins are estimated at between 10% to 15% of the value of cigarettes when they leave the factory (i.e. ex-factory price). By varying these input-price assumptions, we established three retail price thresholds: (1) R21.61, the minimum tax amount that makes no provision for manufacturing or distribution costs, (2) R26.93 (calculated as (18.79 + 2.50) x 1.10 x 1.15), which assumes very low manufacturing costs (R2.50) and industry margins (10%), and (3) R30.14 (calculated at (18.79 + 4.00) x 1.15 x 1.15), which assumes low but viable manufacturing costs (R4.00) and industry margins (15%). The third is our preferred threshold as the first and second are unrealistic because manufacturers would not be making a profit.

Illicit trade: role of informal markets

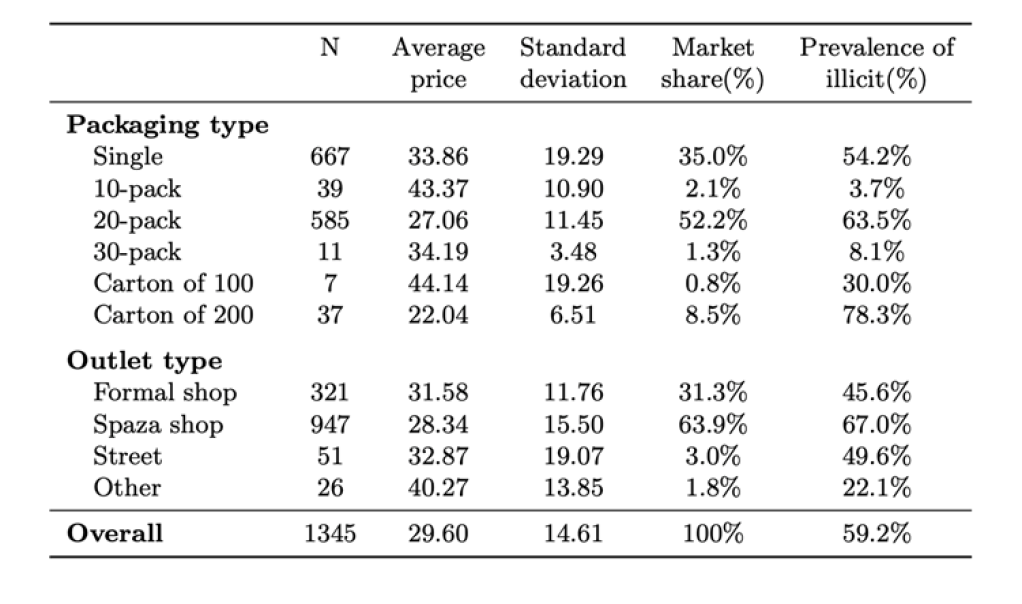

Using the price threshold of R30.14, we find that 59.2% of cigarettes sold in 2021 were illicit (Table 1). The fact that our micro-data-based estimate of illicit trade aligns so strikingly with the macro-level estimate (obtained using gap analysis) gives us strong confidence in the results.

Packs of 20 were the most common packaging type (52.2% of the market), with a 63.5% illicit prevalence, followed by single sticks (35%), with a 54.2% illicit prevalence. The “type of outlet” data reveals that illicit cigarettes were distributed largely through the informal sector, particularly spaza shops—informal, often foreign-owned convenience stores that typically stocks basic necessities—which accounted for nearly two-thirds (63.9%) of all cigarette purchases. Of cigarettes sold at spaza shops, 67% were at prices suggesting they were illicit.

Table 1: Average price per standardised pack and illicit prevalence, by packaging type and by outlet type.

Source: Global Adult Tobacco Survey South Africa, 2021

Furthermore, our regression results (not shown) confirm that purchasing from a spaza shop significantly increases the probability of buying an illicit product. The regression analysis also indicates that illicit cigarette use is more heavily concentrated among unemployed people, low-income earners, and individuals with lower educational attainment.

The Structural Shift: from multinationals to local producers

GATS respondents indicated which cigarette brand they had bought at their most recent purchase. By linking self-reported brands to their producers (based on various online sources), the data allows us to report illicit trade at the brand and producer level.

Historically, British American Tobacco (BAT) has dominated the market, with more than 90% market share in the early 2000s.14 This is no longer the case. The GATS data reveals that, in 2021, BAT’s market share had decreased to 33% (Table 2). Other MNCs collectively held about 8% of the market. Based on the chosen threshold price (i.e. R30.14 per pack), between 13% and 18% of MNCs’ cigarettes were flagged as illicit.

Table 2: Standardised 20-pack price, market share and illicit prevalence, by producer

Source: Global Adult Tobacco Survey South Africa, 2021

By 2021 the market was dominated by non-MNCs. The dominant player is Gold Leaf Tobacco Corporation (GLTC, which rebranded to Polaris Manufacturing in 2025) [15]. GLTC's market share is between 21.2% and 37.7%, positioning it as a direct rival to BAT as the market leader. 85.1% of GLTC’s cigarettes were sold at illicit prices, with an average price of just R23.26 per pack (below both the R26.93 and R30.14 price thresholds). Carnilinx was the third-largest producer, with 10.7% of the market, and an overwhelming 95.9% of its cigarettes were sold below the legal price threshold. Collectively, non-MNCs had 59.1% of the total market share and more than 85% of their volumes were classified as illicit.

Table 3 presents the top 20 brands, with their market shares and illicit prevalence. MNC brands revealed varying prevalence of illicit trade, typically below 14%. BAT’s Peter Stuyvesant (16.2% market share) and Dunhill (6.3% market share) had illicit prevalence of 10.5% and 9.4% respectively, while JTI’s Camel (market share 3%) and PMI’s Marlboro (market share 2.1%) had illicit prevalence of 0.3% and 13.6% respectively.

By comparison, non-MNC brands had extremely high levels of illicit trade; for example, “Remington Gold & RG” (14.5% market share) had an illicit prevalence of 88.8%, and GLTC’s Savannah (6.6% market share) had an illicit prevalence of 94.7%. Other non-MNC brands like Sahawi, Premium, Caesar, and Mega, had nearly a 100% illicit prevalence.

Table 3: Brand prevalence of the top 20 cigarette brands and percentage of illicit.

Source: Global Adult Tobacco Survey South Africa, 2021

Policy Implications: Targeted enforcement and securing the supply chain

The concentration of illicit sales among a group of non-MNC producers suggests tax and law enforcement authorities should intensify their surveillance and compliance interventions among these producers and actively monitor their supply chains.

In August 2022, the South African Revenue Services moved to install CCTV cameras in all cigarette manufacturing and storage facilities. This strategy was successfully opposed in court by the Fair-Trade Independent Tobacco Association, the representative body of various non-MNC producers. Given that our findings identify non‑MNCs as the main suppliers of illicit cigarettes, the irony is hard to miss: the court’s decision effectively protected the manufacturers most responsible for illicit trade from a measure intended to curb it.

The World Health Organization’s Protocol to Eliminate Illicit Trade in Tobacco Products describes various methods to secure the tobacco supply chain. Securing the supply chain entails, among other things, (1) the licencing of all companies involved in the production, import, export and distribution of tobacco products, (2) implementing due diligence on (potential) customers, (3) requiring tobacco companies to keep proper records, (4) implementing a tracking and tracing system independent of the tobacco industry, (5) regulating internet sales and cross-border sales, and (6) having proper control of free trade zones and international transit zones.

The South African government must take urgent steps to address the illicit cigarette trade. Without comprehensive and decisive enforcement interventions, illicit trade will continue to grow, the most vulnerable South Africans will have access to cheap cigarettes, prevalence rates will continue to rise, and government will continue to lose out on tax revenue.

Written by Mxolisi Zondi, Corné van Walbeek & Kirsten van der Zee; Econ3x3

EMAIL THIS ARTICLE SAVE THIS ARTICLE ARTICLE ENQUIRY FEEDBACK

To subscribe email subscriptions@creamermedia.co.za or click here

To advertise email advertising@creamermedia.co.za or click here